Saudi Arabia is a major producer and seller of crude oil as well as the unelected leader of the Organization of Petroleum Exporting Countries (OPEC). Saudi has, in the past, adjusted its production (and thus sale of crude oil) to keep the price  at a level that OPEC desired. For example, if global demand for crude softened, Saudi would cut back production to match demand thus stabilizing the price. The Department of Energy chart shows how Saudi dominates OPEC export sales.

at a level that OPEC desired. For example, if global demand for crude softened, Saudi would cut back production to match demand thus stabilizing the price. The Department of Energy chart shows how Saudi dominates OPEC export sales.

This autumn the demand for OPEC crude fell—but, Saudi decided not to balance supply and demand. Consequently the price of crude oil has dropped to about 50% of what it was at its high in June 2014.

The EIA forecasts the reduced OPEC oil export revenues for 2015 on the following chart:

Shale oil fracking technology has played a significant role in the world’s balance of crude oil supply and demand. The U.S., the major consumer of crude, thanks to fracking now produces more crude than it uses—–no thanks to the US Federal Government that apparently wanted the nation to continue to import crude at higher and higher prices.

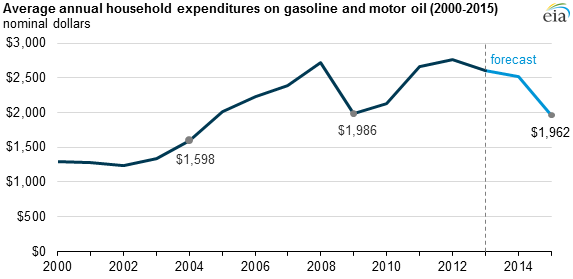

The following chart indicates the forecast fuel savings for an average U.S. household next year:

Saudi intentions as speculated by a number of people reporting on this situation, are manifold. One of their intentions is to put pressure on new fracking as full recovery of costs is often said to require crude prices in the neighborhood of $60 to $80. The existing fracked wells are said to have a variable cost level of around $20 per barrel so they will continue to produce crude.

According to postings on Bloombergview.com by A. Gary Shilling “Ready for $20 Oil?”(posted Dec 21,2014) and ”Who Gets Hurt When Oil Falls?”(posted Dec 22. 2014) Saudi seems likely to have some geopolitical intentions too. Shilling notes that:

“The Saudis also seized the opportunity to damage their opponents, especially Iran and what they see as Iran-dominated Iraq, in the Syria conflict. They also want to help allies Egypt and Pakistan reduce expensive energy subsidies as prices fall.

Then there’s Russia, another Saudi opponent in Syria, with its dependence on oil exports to finance imports and 42 percent of government outlays. With the ruble collapsing, the Russian central bank let the currency float in November after blowing through $75 billion to support it. Then the central bank tried to stop the free fall by raising interest rates by 6.5 percentage points to 17 percent on Dec. 15.

Still, the Russian currency is floundering, along with the economy. Consumer prices in Russia rose 9.1 percent in November from a year earlier. The economy will be in recession next year, the website of the Russian economy ministry acknowledged for a few hours on Dec. 2, before the posting was deleted. “

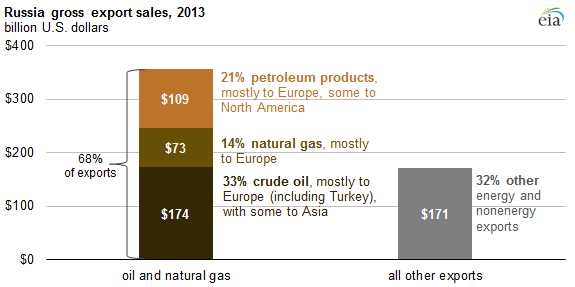

This EIA chart illustrates how important crude oil and crude oil products are as part of Russia’s economy.

Shilling adds:

‘Venezuela is also suffering. The government needs $125-a-barrel oil to cover its spending, of which 65 percent depends on oil exports. Its crude production is down a third since 2000. With inflation raging, the bolivar officially sells for 6.29 a dollar, but for 180 on the black market.”

Are we going to regret this lowering of oil prices? Shilling also has a note of caution for the U.S. when he says:

“I’ve been looking for an economic shock to end the disconnect between soaring equity prices (fueled by central bank largesse) and limping economies. Since the 2008 financial crisis, central bank money has encouraged individuals, businesses and countries to borrow at low rates. The nosedive in oil and other commodity prices makes it hard to pay back those loans as deflation spreads worldwide and almost every currency declines against the U.S. dollar.

The U.S. stock market, while pointing up now, may yet have a negative response to declining energy costs, suggesting that the financial risks from falling oil prices may outweigh the benefits to consumers.

If a full-blown global financial crisis unfolds, along with an accompanying worldwide recession, investment strategy will no doubt shift from the current “risk on” stance to “risk off.” In that scenario, you would expect to see a rush into the safety of Treasury bonds and the U.S. dollar and a stampede out of commodities and stocks globally.

Interestingly, most of this is already in tow. Treasuries are rallying as Americans and foreigners pour in; yields recently hit 2014 lows. The dollar has been robust against the deliberately devalued yen and euro, as well as the currencies of commodity exporters Australia, New Zealand, Canada and Russia. And commodity prices, from oil to copper to sugar, are falling.”

As an observer, the rumored Saudi geopolitical strategy would seem to benefit the U.S. and our allies. The Saudis and some of the OPEC nations are believed to have large savings accounts and can hold out at these low crude oil prices for some long time. But trying to forecast the future some one, two or three years out, if Saudi continues the program that long is beyond my capabilities. Perhaps some of the readers have an insight on how this will play out.

cbdakota

Eat blueberries, they are good for your health.

Pingback: OPEC Strategy Report Says Two More Years Of A Crude Oil Glut | Climate Change Sanity